Buying property can feel exciting until a surprise shows up in the paperwork. Many homeowners learn this lesson the hard way when a lender says, “Your lot touches a FEMA flood zone. You need flood insurance.” Even if it’s just a corner of the land, that one detail can throw off budgets and delay closings. This is where a boundary line survey becomes more than a formality—it becomes your best defense against confusion and unnecessary costs.

The Shock of a Partial Flood Zone

Imagine this: you’re under contract for a house, and everything looks perfect. Then your lender pulls the FEMA maps and finds that a sliver of your backyard, maybe just 10 feet in the corner, touches Zone A. Right away, flood insurance is required. For buyers in Houston, where heavy rain and flooding are real risks, this situation is common.

But here’s the twist—just because part of your boundary is in a flood zone doesn’t always mean your home itself is at risk. That’s the difference most buyers don’t realize until they’re already panicking.

Why Lenders Care About a Sliver of Land

Lenders follow federal guidelines, which say if any portion of the parcel is inside a Special Flood Hazard Area, insurance may be required. It doesn’t matter if the structure sits high and dry. From the bank’s point of view, the rule is simple: reduce risk, protect the loan.

Of course, that leaves buyers feeling frustrated. After all, why should you pay thousands in premiums for a house that’s safe? The answer lies in the documents you provide. And this is where the boundary line survey steps in.

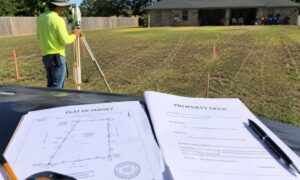

How a Boundary Line Survey Brings Clarity

A boundary line survey defines the exact edges of your property. When surveyors overlay those boundaries on FEMA flood maps, you can see with precision whether the house is inside the zone or if it’s just the land around it. That distinction makes all the difference.

Pairing the survey with a FEMA Elevation Certificate gives lenders and insurers hard proof. The certificate shows your home’s elevation compared to the Base Flood Elevation (BFE). If your finished floor sits above the BFE, you may be able to lower or even challenge the insurance requirement.

Houston’s Unique Flood Challenges

Houston’s landscape makes this issue even more important. With bayous, creeks, and flat terrain, small changes in elevation can shift the risk dramatically. Harris County Flood Control District (HCFCD) tools, like the Flood Education Mapping Tool (FEMT) and MAAPnext, give residents access to detailed maps. But without a surveyor, most people can’t tell if their property’s official line clips into a hazard zone.

In other words, the maps raise questions—but the survey provides answers.

From Reddit Panic to Houston Playbook

Over the past week, threads on Reddit have been full of Houston buyers asking, “Should I walk away if a corner of my lot is in Zone A?” Others share frustration over sudden premium hikes, especially as NFIP updates roll out. These conversations show how common the problem is, but also how misunderstood.

Here’s the reality: walking away isn’t the only option. A smart plan can save your deal.

- Check the maps yourself. Use FEMT and MAAPnext to see if the effective or preliminary maps show overlap.

- Hire a licensed land surveyor. A professional boundary line survey confirms exactly where the parcel and structures sit.

- Get an Elevation Certificate. This document shows if the home is actually above flood risk.

- Consider a LOMR-F (Letter of Map Revision – Removal). If the house itself is safe, FEMA may officially remove it from the flood zone, even if part of the lot stays in.

- Talk with your lender. Share the documents and ask for reconsideration. In many cases, better data leads to better outcomes.

What to Say to Your Lender or Insurer

If you’re stuck in this situation, communication is key. Here’s a short message you can adapt:

“Enclosed is my boundary line survey and FEMA Elevation Certificate showing that the lowest floor of my home is above the Base Flood Elevation. Please confirm if this qualifies for reduced or waived flood insurance requirements.”

Simple, clear, and backed by professional documentation—this approach gives your lender something solid to review instead of vague arguments.

Real Savings from Surveys

The value of this process goes beyond peace of mind. In Houston, homeowners have used boundary line surveys and elevation certificates to:

- Prove their homes sit higher than the mapped flood zone.

- Secure lower flood insurance premiums.

- Avoid unnecessary insurance when FEMA approves a map revision.

- Close deals that might have fallen apart without documentation.

Flood insurance can cost thousands every year. Spending on a survey and certificate once can pay for itself many times over.

When You Shouldn’t Skip It

Not every property touches a flood zone, but growth makes the odds higher. If you’re buying near bayous, creeks, or low-lying neighborhoods, don’t gamble. A boundary line survey gives you leverage during due diligence and at closing. Even if your lender won’t waive insurance, you’ll at least know you’re paying for coverage you actually need, not just because of a technicality.

Final Thoughts

Flood zones aren’t going away. In fact, with new FEMA maps on the horizon, more properties may find themselves affected. The good news is you don’t have to panic if a corner of your lot touches Zone A. A boundary line survey can show where your land and structures really sit, and an Elevation Certificate can prove whether your home is truly at risk.

So if you’re facing that stressful call from your lender, don’t walk away just yet. Talk to a licensed surveyor, get the facts, and put the right documents on the table. The difference between rumor and reality might save you thousands—and protect the home you’ve already fallen in love with.